China’s Economy Staggers Again Under Domestic Demand Shock, Stimulus Dilemma Deepens for Debt-Laden China

Authored On

Modified

China’s economy flashes warning signs again as retail sales growth hits lowest level in 3 years and 4 months Property recovery remains distant, raising pressure for additional policy support amid deteriorating conditions Effectiveness of stimulus measures questioned as debt-dependent growth model shows mounting strain

Fresh warning signals have emerged across the Chinese economy just as signs of recovery had begun to surface. Consumption, industrial output, and investment all weakened simultaneously, rapidly extinguishing optimism surrounding the first-quarter rebound within the span of a single month. Markets are closely watching the possibility that the People’s Bank of China (PBOC) may roll out aggressive stimulus measures, including benchmark rate cuts and further reductions in reserve requirement ratios. Yet the core issue lies less in liquidity shortages than in the collapse of consumer and investment confidence. After decades of relying on debt accumulation and property development to sustain growth, China now appears increasingly trapped in a prolonged deflationary spiral in which additional monetary easing merely fuels further debt expansion.

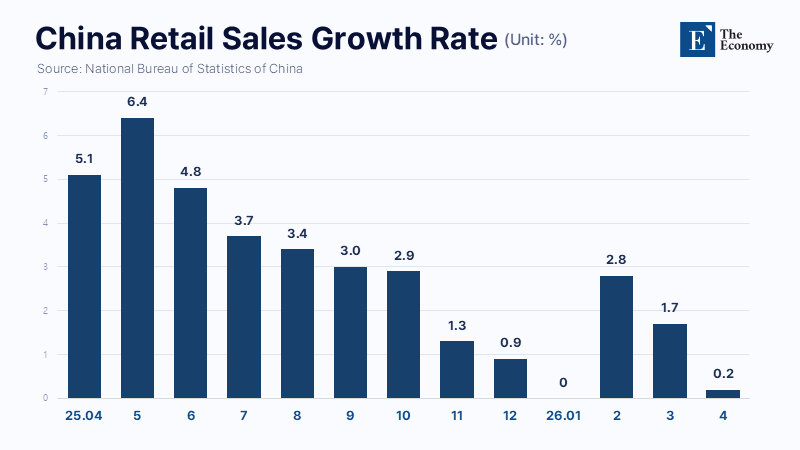

Retail Sales Growth Falls to 0.2%, Domestic Demand Effectively Stagnant as Property Investment Plunges 13.7%

According to China’s National Bureau of Statistics on May 19, key economic indicators including April retail sales, industrial production, and property investment all delivered severe downside surprises, falling well short of market expectations. The most striking figure was retail sales growth, a key gauge of household consumption sentiment, which collapsed to just 0.2% year-on-year. That marked a sharp slowdown from March’s 1.7% expansion and came dramatically below the market consensus forecast of 2%. On a growth-rate basis, it represented the weakest reading since December 2022, when retail sales contracted 1.8%, marking a 3-year-and-4-month low.

Industrial production rose just 4.1% year-on-year. That was sharply weaker than March’s 5.7% increase and far below economists’ expectations of 6%. It also marked the weakest growth pace since July 2023, when output expanded 3.7%. On a month-on-month basis, industrial production rose only 0.05%, effectively signaling stagnation. Analysts pointed to the energy shock triggered by the Iran war as a major factor behind the slowdown. Surging oil prices and supply instability raised corporate cost burdens, yet weak domestic demand prevented companies from fully passing those costs on through higher prices.

The property downturn also continues to deepen. Property development investment between January and April fell 13.7% from a year earlier, underscoring that the restructuring shock unleashed after the Evergrande crisis has yet to run its course. Total fixed-asset investment during the same period also declined 1.6%, undershooting market forecasts. After rising 1.7% in the first quarter and showing tentative signs of stabilization, investment returned to contraction within a single month. By sector, investment in primary and secondary industries rose 10.1% and 2.5%, respectively, while investment in the tertiary sector fell 4.2% during the same period.

Economists increasingly interpret the latest figures as evidence of a full-scale domestic demand shock. Until the first quarter, sentiment surrounding China’s economy had remained relatively optimistic, with many analysts arguing that growth was proving “stronger than expected.” China’s first-quarter gross domestic product (GDP) expanded 5% year-on-year, while industrial production rose 6.3% during January and February and 5.7% in March, reinforcing confidence in the manufacturing sector. Yet April’s data now suggests that first-quarter momentum is fading rapidly as the second quarter begins. The slowdown in investment is particularly pronounced within the private sector, intensifying policy concerns in Beijing. Private-sector investment between January and April declined 5.2% year-on-year. Even excluding real estate, private investment still contracted 1.9%. The figures stand in stark contrast to continued investment growth in high-tech industries and aerospace manufacturing sectors that remain heavily supported by the Chinese government.

Household Lending Contracts Despite Property Stabilization as Income Anxiety Drives Deleveraging

The deepest fracture within China’s economy stems from the erosion of price expectations. Producer prices have faced persistent downward pressure for an extended period, while consumer inflation has continued to undershoot official targets. Although producer prices recently rebounded temporarily due to Middle East-driven energy shocks, rising prices are more likely to function as an additional cost burden than as a signal of economic recovery so long as domestic demand remains weak.

Deflationary psychology is also fundamentally altering consumer spending behavior. Even as parts of China’s property market show tentative signs of stabilization, household credit indicators are moving in the opposite direction. According to the National Bureau of Statistics, prices for newly built homes in China’s tier-one cities — including Beijing, Shanghai, Guangzhou, and Shenzhen — rose 0.1% month-on-month in April, while existing home prices climbed 0.4%. Nationwide housing transaction volumes also increased 13.4% year-on-year during April.

However, PBOC data showed outstanding yuan-denominated loans unexpectedly contracted by approximately $1.4 billion in April, marking a rare negative reading. Household loans declined by approximately $109 billion during the same month, representing an additional contraction of roughly $36.8 billion compared with a year earlier. Short-term loans fell approximately $61.5 billion, while medium- and long-term loans declined roughly $46.9 billion, confirming weakening demand across both consumer finance and mortgage lending.

China’s greatest economic challenge is therefore fundamentally a demand shortage. Supply-side capacity remains robust, yet consumer and investment sentiment continues to deteriorate. Even the National Bureau of Statistics recently acknowledged publicly that “domestic demand remains relatively weak.” Against that backdrop, analysts increasingly expect Beijing to fall back once again on fiscal expansion and monetary easing. Markets had previously expected the PBOC to hold interest rates steady for the time being in order to defend banking sector margins, in line with forecasts from institutions such as OCBC. However, the severity of April’s economic shock may now force a complete reassessment. To prevent a hard landing, the PBOC could soon deploy major stimulus measures, including cuts to the Loan Prime Rate (LPR), China’s benchmark lending rate, or additional reserve requirement ratio reductions aimed at injecting large-scale liquidity into the financial system.

China Buried Under Debt as Combined Government, Corporate, and Household Debt Surpasses 300% of GDP

Yet monetary easing alone is unlikely to revive domestic demand. Rebuilding household safety nets, reforming pensions, healthcare, and social security systems, restructuring local government finances, and restoring private-sector confidence must all proceed simultaneously. China also faces growing pressure to shift toward a productivity- and innovation-driven industrial structure. Companies must generate sustainable profits that can ultimately flow into household income if consumption is to recover. Most importantly, the essence of China’s current crisis lies in the collapse of a growth model built over decades on debt-fueled expansion and property speculation. As the asset bubble created through massive development projects and aggressive borrowing deflates, the accumulated debt burden is increasingly being transferred directly into the real economy.

China’s combined government, corporate, and household debt reached 302.3% of GDP as of the third quarter of last year. According to the National Institution for Finance and Development, a think tank under the Chinese Academy of Social Sciences, the country’s total debt ratio remained in the 240% range between 2016 and 2019 before surging into the 270% range in 2020. By the end of 2024, the ratio had climbed to 287.1%, rapidly approaching the 300% threshold. At the current pace, China’s total debt burden likely exceeded 300% of GDP on a full-year basis in 2025 for the first time in history. Total outstanding debt stood at approximately $55 trillion as of the end of the third quarter last year.

Several factors have contributed to the rapid rise in China’s debt ratio. One major driver has been the enormous fiscal resources deployed by Beijing to address the long-standing issue of hidden local government debt. China has been pursuing a decade-long cleanup campaign targeting hidden debt since 2018. However, after economic growth weakened sharply beginning in 2021 and local government finances deteriorated rapidly, Beijing increasingly opted to shift repayment burdens away from local authorities by expanding central government borrowing. That dynamic explains the particularly sharp rise in government-sector debt ratios.

Local government bond issuance also accelerated as Beijing ordered authorities to dismantle so-called shadow financing structures — non-bank financial activities operating outside formal regulatory oversight. Local governments rushed to issue bonds in order to resolve liabilities held within Local Government Financing Vehicles (LGFVs). However, after Chinese authorities intensified efforts last year to contain financial instability tied to shadow banking, local bond issuance surged even more aggressively. According to estimates from the International Monetary Fund (IMF), LGFV debt in China has reached approximately $8.4 trillion, more than four times higher than the roughly $2 trillion officially reported by Beijing. China’s actual debt burden is therefore believed to be substantially higher than official figures suggest.

Under such conditions, additional stimulus measures may temporarily stabilize headline indicators while simultaneously magnifying long-term vulnerabilities. Aggressive easing implemented against a backdrop of deteriorating economic fundamentals risks exhausting the government’s remaining policy tools without resolving underlying structural problems. More critically, expanding public debt further may ultimately fuel inflationary pressures and rising unemployment through higher interest-rate burdens. Beyond stronger economic growth capable of expanding tax revenues and reductions in welfare expenditures, few viable options remain for reducing public debt burdens over the longer term.

- Previous “Beyond Smartphones to AI Servers” LPDDR Emerges as the Next Memory Battleground After HBM, With Prices Poised to Rise as China’s Catch-Up Effort Falters

- Next U.S. Strategic Recalibration Around Greenland’s ‘Unsinkable Aircraft Carrier,’ Pivoting From Annexation to Expanded Military Footprint With Russia-China Containment at Core

Similar Post