“Time for Tightening?” Middle East-Driven Inflation Shock Sends U.S. Long-Term Treasury Yields Surging, Complicating Prospects for Rate Cuts Under a Warsh-Led Fed

As one of the youngest members of the team, Tyler Hansbrough is a rising star in financial journalism. His fresh perspective and analytical approach bring a modern edge to business reporting. Whether he’s covering stock market trends or dissecting corporate earnings, his sharp insights resonate with the new generation of investors.

Authored On

Modified

Middle East conflict fuels inflation fears, driving prolonged rally in U.S. long-term Treasury yields Shockwaves spreading into the real economy through rising mortgage rates and mounting corporate losses Fed under incoming Chair Kevin Warsh seen facing limited room for near-term monetary easing

U.S. long-term Treasury yields are staging a sharp ascent. As the Iran war intensifies global inflationary pressures, markets have begun pricing in the prospect of prolonged monetary tightening. With war-driven risks rapidly spilling beyond financial markets into the broader real economy through higher mortgage rates and rising corporate funding costs, investors are increasingly focused on the monetary policy direction of incoming Federal Reserve Chair Kevin Warsh as the decisive variable shaping the next phase of the cycle.

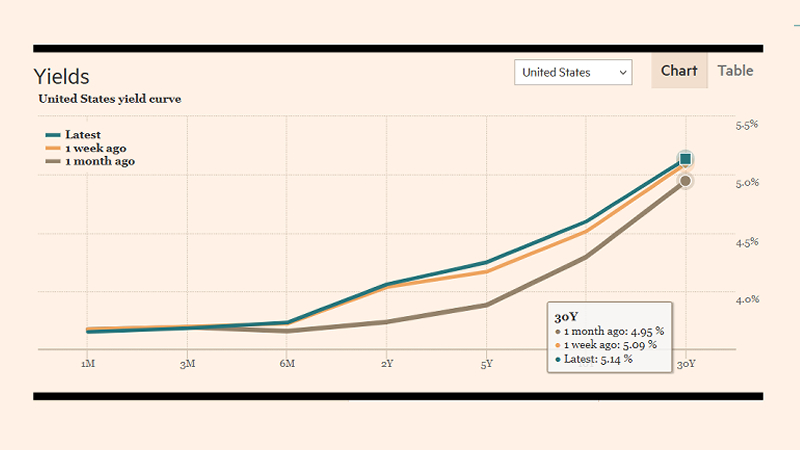

Volatility in U.S. Long-Term Treasury Yields

According to Bloomberg on May 18 (local time), the yield on the benchmark 10-year U.S. Treasury note climbed above 4.60% intraday, reaching its highest level in roughly 15 months. The yield on the 30-year Treasury bond also surged to as high as 5.16% during trading. After breaching the 5.1% threshold on May 15 for the first time since July 2007, the long-end selloff has continued unabated. The move stands in stark contrast to shorter-dated Treasuries, where 1- and 2-year yields have remained relatively contained around the 4% range. The divergence suggests markets are increasingly focused on the risk of structurally higher rates over the long term rather than immediate tightening measures.

The Middle East conflict is widely viewed as the principal catalyst behind the surge in long-term Treasury yields. The Strait of Hormuz, a strategic chokepoint through which roughly 20% of global oil shipments pass, has remained effectively blocked since the United States and Israel launched preemptive strikes against Iran in late February. International crude prices have consequently hovered near $100 per barrel for months. At the same time, a sharp decline in tanker traffic through the Middle East has triggered a spike in shipping freight and insurance costs, while logistical bottlenecks across the region have driven up prices for plastics, fertilizers, and chemical products. The result has been an intensification of global inflationary pressures.

Against this backdrop, U.S. inflation indicators accelerated sharply last month. Consumer Price Index (CPI) inflation rose 3.8% year-over-year, marking its highest level since 2023. Energy prices surged more than 17%, while food, airfare, and housing costs also posted pronounced increases. Over the same period, the Producer Price Index (PPI) jumped 6%, the largest increase since 2022, with energy and chemical products accounting for the bulk of the rise.

Warning Signals Across the Real Economy

The market shock generated by the war is now visible beyond bond yields and inflation data. According to the Financial Times, the average U.S. 30-year mortgage rate recently climbed to 6.36%. The rise came despite directives from the Donald Trump administration instructing government-backed agencies to purchase mortgage-linked securities in an effort to stabilize borrowing costs, with the effects of the conflict largely overwhelming policy support. Bradley Saunders of Capital Economics said, “As long as mortgage rates remain above 6%, it will be difficult for the U.S. housing market to generate a meaningful recovery.”

Similar patterns are emerging across Europe. Mortgage rates in Germany, the eurozone’s largest economy, recently rose by roughly 0.3 percentage points, with 10-year home loan rates climbing to around 3.6%. In the United Kingdom, the average two-year fixed mortgage rate for loans with a 75% loan-to-value ratio surged from 3.97% in late February to 5.1% last month. As expectations spread that central banks will be forced to raise benchmark interest rates in response to intensifying inflation pressures, borrowing costs are beginning to rise in earnest.

Industry is also being thrown into deep disarray. Reuters reported on May 18 that companies worldwide have already suffered at least $25 billion in losses as a result of the Iran war. The figure was compiled using disclosures and earnings data from listed firms across the United States, Europe, and Asia following the outbreak of the conflict. According to Reuters’ analysis, at least 279 companies have either raised prices or cut production in an attempt to offset the financial damage caused by the war. Some firms in the heavily affected airline sector have suspended dividend payments and share buybacks or temporarily laid off workers. In some cases, fuel surcharges have been introduced, while other companies have sought emergency government assistance.

Direction of Fed Monetary Policy

Amid these developments, global attention is increasingly centered on Kevin Warsh, who is set to officially assume the role of Federal Reserve chair this week. Warsh has consistently argued that productivity gains driven by artificial intelligence (AI) could offset inflationary pressures, making monetary easing necessary. His stance has broadly aligned with President Trump, who has spent years pressuring the Fed to cut rates. Trump repeatedly urged former Fed Chair Jerome Powell to pivot monetary policy after Powell maintained an extended pause on rate cuts. Last month, Trump also remarked that he would be disappointed if Warsh failed to move toward rate cuts immediately after taking office.

Even so, markets overwhelmingly expect the Fed to maintain a restrictive stance for an extended period even under Warsh’s leadership. Mounting inflationary pressure and rising Treasury yields have begun constraining expectations for policy easing. On prediction market platform Kalshi, the probability that the Fed cuts rates before 2027 is currently priced at roughly 38%, down sharply from around 96% in February. CME FedWatch data shows a 98.8% probability that the Fed keeps benchmark rates unchanged through the end of June, while the probability of rates remaining on hold through July is also estimated at above 94%.

Within the Fed itself, sentiment has gradually shifted in a more hawkish direction. Reports indicate that significant divisions emerged among Federal Open Market Committee (FOMC) members during last month’s meeting regarding the possibility of additional tightening. Four officials reportedly dissented from the decision to hold rates steady, with some warning that surging oil prices could evolve into entrenched long-term inflationary pressures and even raising the prospect of further rate hikes. The discussion suggests growing recognition inside the central bank that the Middle East conflict could evolve from a temporary shock into a broader inflationary threat capable of feeding into wages and service-sector prices.

As one of the youngest members of the team, Tyler Hansbrough is a rising star in financial journalism. His fresh perspective and analytical approach bring a modern edge to business reporting. Whether he’s covering stock market trends or dissecting corporate earnings, his sharp insights resonate with the new generation of investors.

- Previous “AI-Driven Power Crisis Reshapes Market Landscape” NextEra Pursues Dominion Acquisition as M&A and Capital Spending Surge Across U.S. Power Sector

- Next [U.S.-Iran Peace Talks] “Military Strike on Iran Put on Hold” U.S. Maintains Military Pressure Amid Nuclear Deadlock as Focus Shifts Toward ‘Economic Negotiations’ Before the Storm

Similar Post