Critical Minerals Security Reform

Ethan McGowan is a Professor of AI/Finance and Legal Analytics at the Gordon School of Business, SIAI. Originally from the United Kingdom, he works at the frontier of AI applications in financial regulation and institutional strategy, advising on governance and legal frameworks for next-generation investment vehicles. McGowan plays a key role in SIAI’s expansion into global finance hubs, including oversight of the institute’s initiatives in the Middle East and its emerging hedge fund operations.

Authored On

Modified

Low cost alone no longer guarantees stability in global markets Critical minerals security has become the foundation of industrial credibility Restoring open trade now requires rebuilding trust in supply continuity

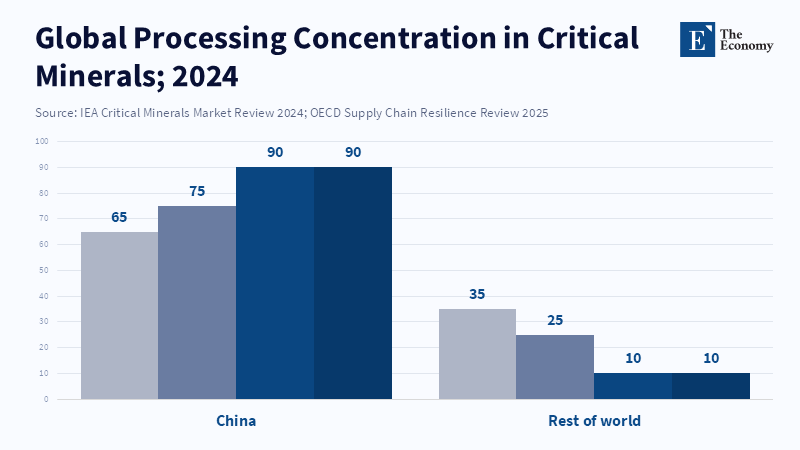

The core lesson from recent history is clear: when supply is cut off, access is more important than getting the lowest price. During 2024 and 2025, policy changes and logistical problems transformed key minerals from cheap materials into strategic points of control. These points can stop car production, delay deliveries in the defense sector, and slow down the introduction of green energy. Currently, China handles most of the refining and processing in the mineral value chain that powers much of modern manufacturing. It often controls over two-thirds of the market at many intermediate stages, and this share reaches 90% in magnet production and separation. This level of control means that a simple policy change or a delay in licensing can quickly change the dynamics of global production. The short-term advantages of moving production overseas are then negated by long and costly disruptions. The important question for policymakers is not just whether markets decide how resources are allocated, but whether the belief in markets—the assurance of a steady supply—can be restored. The answer is to start treating the security of critical minerals as the public benefit they have become.

Why Basic Economics Doesn't Work for Critical Minerals Security

The discussion needs to be readdressed. For years, the idea of producing goods where costs are lowest has been almost untouchable. Businesses moved production to locations where they could pay the least per item, assuming markets would remain open and predictable. This plan fails because a small number of producers control refining, processing, or vital parts. If a country or business can stop the flow of these items without harming itself much—or threaten to do so convincingly—the basic idea that markets always share things out well falls apart. The key problem isn't just the usual external factors that affect everyone; it's that trade chokepoints are used for political purposes. When it is not certain that supplies will continue, price signals are no longer enough to guide investments and planning.

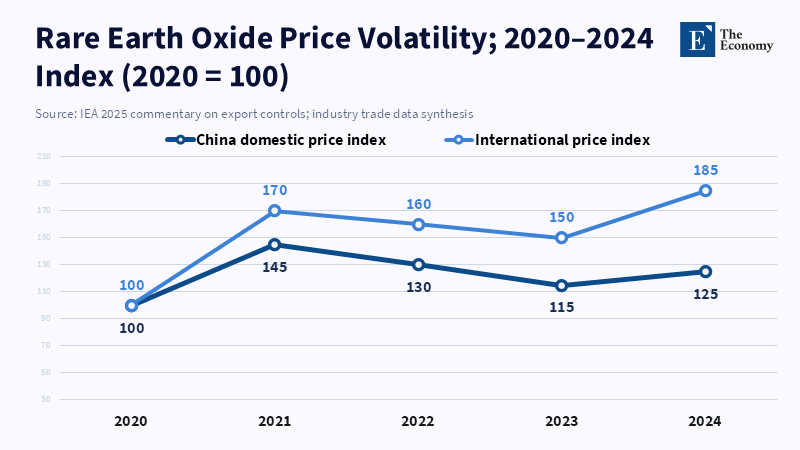

This is important now because real-world details show that this failure is not just theoretical. From 2024 to 2025, export restrictions and new industrial rules combined to make the supply of key minerals unstable. The International Energy Agency and other experts have shown how shifts in policy and the concentration of refining have caused immediate, noticeable problems, such as higher prices outside the main supplier and slower production in related industries. Companies that planned their processes around securing today's lowest prices were the ones that suffered most when future supplies were cut off. Policymakers are confronting a realization: The choice used to be between cost and overall well-being, but now it also includes whether supply chains are reliable or prone to unexpected disruptions. This changes how we calculate what is best for the overall economy.

The immediate policy suggestion is that basic economics, which assumes trade is smooth and apolitical, requires something more. Markets run smoothly if rules are believable and organizations can enforce them. But believability is cheap only if supply chains are spread out, and no single country or business has too much control. When control exists, governments need to consider constant access to these materials as a separate, important element for society. This doesn't mean getting rid of markets, but it means adding security measures into how markets are set up, how purchases are made, and where public money is invested. The goal is to bring back a reliable expectation that supply will not be cut off so that price again becomes a helpful guide for private investments.

Actionable Plans to Reestablish Security for Critical Minerals

If the main concern is a stable, consistent supply, the approach must be varied, quick, and precisely aimed. Three important policy supports stand out: maintaining strategic reserves and rotating them, forming strong industrial partnerships, and using targeted market incentives to encourage production closer to home and diversification among allies. No method works by itself, but together they can bring back dependability to markets.

First, keeping strategic reserves is not a perfect solution, but it provides time and reassures the industries. Unlike unplanned hoarding, a smart reserve program is open, rule-based, and rotates materials through business channels so they don't spoil or become obsolete. The amount stored should match the degree of geographic concentration of the sources and the sensitivity of downstream demand. For instance, if refining or magnet-making is focused in a single country, maintaining a six- to twelve-month supply of key magnet materials can prevent factories from shutting down while projects to expand the supply chain get started. These reserves must be measured and audited in public to stabilize market assumptions. Evidence from recent export restrictions shows that even small, carefully managed reserves can soften price surges and prevent production halts.

Second, creating industrial partnership networks, through organized alliances for co-investment between two or more countries, is crucial. The goal is not to rebuild every production stage at once, which would waste money, but to create separate centers dedicated to keeping supply lines open. Coalitions of similar democratic countries can support shared refining plants, joint processing businesses, and agreements for mutual licensing assistance that only take effect during specific crises. These setups change the incentives for those in the leading supplier country: If restricting exports only shifts business to partner-nation refineries without seriously hurting overall demand, there is little political usefulness in using supply as a weapon. Improving skills and abilities across multiple countries also helps new projects get off the ground faster by sharing technical knowledge and speeding up the permitting process, two common problems for locating businesses closer to home.

Third, market tools must be reevaluated to account for supply security. This means using short-term, clear price supports or guaranteed purchase agreements that reduce the risk of investing in new processing abilities outside the main supplier. These tools can be designed to be conditional and phased out once the countries have a diverse industrial base. Policymakers should avoid creating permanent protections; instead, they should use short, credible support periods to address coordination failures that prevent private investors from funding refining and separation facilities. For example, a blended finance system that links loan guarantees with temporary price support can lower the average cost of capital enough to make new plants worth funding in areas with strong economic conditions.

Addressing Common Criticisms

Any effort toward security, even on a small scale, brings familiar criticisms: it will raise prices for consumers, spark retaliation, and reignite the old argument over protections versus open markets. These are valid concerns, but need careful consideration in context.

Looking at the cost issue: Yes, making supply more secure raises unit costs in the short run. Businesses that sought the cheapest supplies earlier will see their profits change. But the alternatives matter. The alternative involves price swings, production halts, and little investment, all of which impose greater, more unfair costs on society over time. Recent cases show that sharp price increases can be large and lasting if triggered by supply issues. On the other hand, clear, temporary actions tend to narrow the range of future prices and promote early investment, thereby lowering long-term costs. When the government accounts for the security premium through calculated, temporary support, the total social cost can be lower than the combined losses from frequent disruptions.

Regarding retaliation, countries with significant market control can respond. The risk, though, is not equal. If diversification and shared investment among allies create credible alternative supply sources, the control that a single country can exert is weakened. Diversification reduces the value of using coercive methods for the country, given the considerations. This might not eliminate diplomatic risk, but it alters the decision-making: coercion becomes more costly and less likely to produce lasting gains.

The idea that this suggests abandoning free trade misunderstands the point. The policy framework I am suggesting is not a rejection of openness. It is an adjustment made for practical reasons. We accept the social benefits of international production, but we insist that the system assures a minimum level of continuity in essential supplies. Markets should still decide who produces what, but governments must confirm the underlying system is reliable enough for market results to matter. This is about governance, not a denial of economic principles.

We are past the point of arguing that low cost is always the most important factor. Experience shows that when only a few participants control processing and the politics around supply intensify, markets stop being a reliable means of maintaining industrial stability. Restoring Basic Economics is possible, but it requires restoring one key element: reliable, continuous access to essential supplies. This requires a practical set of tools, involving audited reserves, multilateral co-investment in processing, and time-limited market supports that decrease investment risk for diversification. Policymakers must act now with focus and clarity. Security measures must be clear, temporary, and precisely targeted so they do not become protectionist policies. We can re-anchor global markets on a stable supply structure, and price signals will then enable practical outcomes once again. If this goal cannot be reached, the discussion will no longer be about free trade versus protection, but about who decides whether factories run or grids stay powered. The choice is both immediate and structural. Critical minerals security must be considered as infrastructure, meaning the old economics can be restored with a stronger set of rules that make markets reliable once more.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Chatham House (2025) Kynge, J., China’s new restrictions on rare earth exports send a stark warning to the West. Chatham House, Expert comment, 10 October 2025.

China Briefing (2025) Huld, A., Rare Earth Elements: Understanding China’s Dominance in Global Supply Chains. China Briefing, 29 August 2025.

IEA (2025) Kim, T.-Y., Dhir, S., Dasgupta, A. & Scanziani, A., With new export controls on critical minerals, supply concentration risks become reality. IEA, 23 October 2025.

OECD (2025) Arriola, C., Bates, O., Cai, M., Chiapin Pechansky, R., Ferencz, J., Fiorini, M., Jaax, A., Kowalski, P., Lopez Gonzalez, J., Miroudot, S., Sorescu, S., Tresa, E. (2025) OECD Supply Chain Resilience Review. OECD Publishing.

Reuters (2026) Howe, C. and Lee, L., China imposes export controls on 20 Japanese entities to curb ‘remilitarisation’, Reuters, 24 February 2026.

East Asia Forum (2026) Eggert, R.G., Critical minerals and the reimagination of globalisation. East Asia Forum, 22 February 2026.

East Asia Forum (2026) Zhang, M.Y., Way out of the West’s critical minerals dilemma. East Asia Forum, 22 February 2026.

Ethan McGowan is a Professor of AI/Finance and Legal Analytics at the Gordon School of Business, SIAI. Originally from the United Kingdom, he works at the frontier of AI applications in financial regulation and institutional strategy, advising on governance and legal frameworks for next-generation investment vehicles. McGowan plays a key role in SIAI’s expansion into global finance hubs, including oversight of the institute’s initiatives in the Middle East and its emerging hedge fund operations.