Rebuilding Growth: Why China’s Next Decade Is About China rebuilding capital, not a quick rebound

Keith Lee is a Professor of AI/Finance at the Gordon School of Business, part of the Swiss Institute of Artificial Intelligence (SIAI). His work focuses on AI-driven finance, quantitative modeling, and data-centric approaches to economic and financial systems. He leads research and teaching initiatives that bridge machine learning, financial mathematics, and institutional decision-making.

He also serves as a Senior Research Fellow with the GIAI Council, advising on long-term research direction and global strategy, including SIAI’s academic and institutional initiatives across Europe, Asia, and the Middle East.

Authored On

Modified

China’s slowdown reflects a long process of rebuilding capital after a debt-driven boom The shift from property to technology will be slow and uneven Durable growth now depends on repair, reform, and smarter capital use

China’s boom years were built on borrowed money, borrowed confidence and borrowed buyers. Today, those loans are being repaid, written down, or quietly rolled over — and the gap they leave is large. The single, hard number that frames the moment is this: even as Beijing pushed fiscal and credit support in 2024–25, the country ran a record trade surplus in 2025, exceeding US$1 trillion — a sign not of overheating demand at home but of external engines carrying what domestic capital flows and household spending no longer can. China isn't simply “slowing” and waiting for a policy fix. It is undergoing a wholesale rebuilding of capital — repairing balance sheets, reconstituting public and private investment models, and trying to fund tomorrow’s factories and AI labs with endogenous resources rather than the unceasing expansion of land-backed credit that powered the past. That task is long, uneven and politically costly. It will shape what educators, administrators and policymakers need to prepare for: slower-but-different growth, persistent labor-market churn, and renewed pressure to convert physical and financial capital into human capital and institutional capability.

China rebuilding capital: what the loss of leverage means for growth

The conventional narrative treats China’s slowdown as a cyclical shortfall: cut taxes, loosen credit, restart construction and consumption returns. That story misses the deeper arithmetic. During the bubble years, the economy relied heavily on credit-fueled property development and local-government land sales to create new capital stock and household wealth. As those sources evaporate, the economy can no longer count on rapid capital accumulation to produce fast GDP growth. Instead, it faces a multi-year accounting process: losses must be recognized, bad loans must be provisioned, equity must be written down, and public guarantees must be partially restored or phased out. During that interval, measured investment will be lower. Measured GDP will grow more slowly. That is not a policy failure to “stimulate” quickly; it is the natural lag while the economy digests past over-leverage and rebuilds sustainable capital — a process that is essentially mechanical and time-consuming.

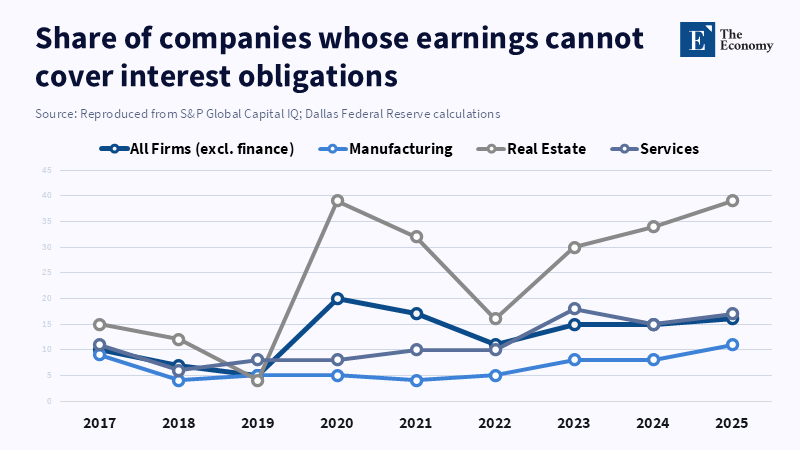

The scale of the property correction makes this especially concrete. Analysts estimate tens of millions of unsold or effectively vacant housing units across the country; one respected analysis places that figure near eighty million homes as the slump approached its fifth year. Those unsold units are not neutral statistics — they are capital that fails to generate returns, collateral that cannot easily support new borrowing, and a wealth shock to households whose consumption decisions rest on perceived asset values. As developers and lenders shrink balance sheets to reality, fewer new projects move forward, construction jobs disappear, and local government revenues tied to land transactions fall. All of this lowers public and private capacity to reinvest quickly.

How long will the rebuilding take? Lessons from history and the numbers

When a growth model pivots from externally or credit-driven capital formation to internally funded, productivity-led investment, time horizons matter. Japan’s 1990s correction is the cautionary exemplar: when a large property and equity bubble collapsed, Japan spent much of a generation recognising losses, recapitalising banks and rerouting resources — a process that included repeated fiscal and banking interventions yet still produced decades of subpar growth relative to earlier trends. The banking system absorbed enormous amounts of non-performing loans; a careful accounting shows the official fiscal and banking costs related to cleanup ran into the tens of percent of GDP over the 1990s. Those are not exact templates for China, but they show that balance-sheet repair is slow and that growth frequently normalises at a lower headline pace during the transition.

For China, the arithmetic is further complicated by recent increases in the total debt stock. Augmented measures of Chinese debt — public, corporate and household combined — climbed in the early 2020s, and the ratio to GDP continued to rise in 2023 and 2024. That higher starting point means more of the near-term output must be devoted to servicing and restructuring liabilities before capital formation returns to pre-crisis intensity. International institutions tracking China’s macro profile in 2024–25 consistently flagged this constraint and projected growth rates for 2025–26 that were lower than the boom years but still positive, showing a mix of modest fiscal support and continued export demand. Those proprojections showrealistic midpoint: repair, not rebound; reallocation, not rapid replication of past patterns.

Policy pivots: why ‘fixing’ growth means re-anchoring capital, not pumping it

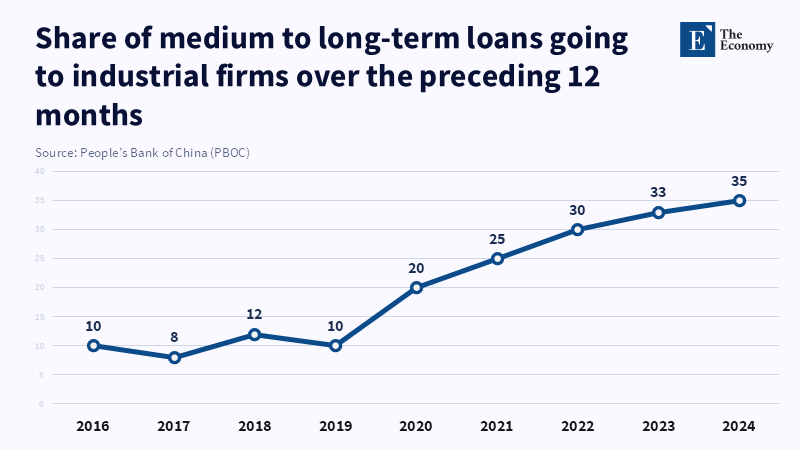

Faced with falling property-driven capital and weaker household wealth, Beijing has been explicit about a strategy of “high-quality growth.” That means shifting public support toward technology, green energy and advanced manufacturing, and away from indiscriminate credit to land and real estate. Think tanks and regional macro offices document a sa spike in directed investment and subsidies in these priority sectors, even as aggregate investment growth is sluggish. This is not simply a change in sectoral taste. It is an attempt to reconstitute the nature of capital in the economy: from an asset-heavy, low-return stock of housing and land to a portfolio emphasizing R&D, equipment, software, and skills. MERICS

That pivot has an evident tension. Building human capital and technology capability takes longer than approving a new residential project. It requires regulatory clarity, education and training, and patient capital that may produce returns on a far longer horizon. Meanwhile, overcapacity risks remain in some of the very “new economy” sectors Beijing prizes; public subsidies and industrial planning have, in several cases, already led to output exceeding domestic demand. Good policy here means two things at once: managing excess capacity where it exists and ensuring that the scarce public resources used to seed future sectors are tightly targeted, conditional, and linked to skills development and market requirements. Recent institutional analyses have shown that unchecked subsidies risk recreating the same distortion — a different set of white elephant factories rather than durable, knowledge-driven capital.

What educators, administratorand policymakers need to do now

The transition from leveraged, asset-heavy growth to a capital base oriented around skills, technology and services creates concrete tasks for education systems and public policy. First, curriculum and training must shift away from funneling graduates into short-term construction and local-government patronage roles toward technical and managerial skills that support high-value investment. That means scaled vocational training that is genuinely tied to employers, robust lifelong learning pathways for mid-career workers, and incentives for firms to invest in on-the-job training. Second, public finance must be designed to crowd in private patient capital for R&D and equipment upgrades, and to include outcomes measures and sunset clauses for subsidies so that they do not preserve inefficient producers. Third, safety nets matter: slower capital formation will translate into periods of weak wage growth and employment churn. Effective unemployment supports, retraining vouchers and portable benefits will reduce the social cost of the restructuring and make labor markets more flexible. AMRO and other regional observers note these points in projecting a medium-term path for China that is steadier but not as rapid as the bubble years. AMRO

Anticipated critiques will say this is too slow, that deliberate repair will choke growth and undermine social stability. The counter is pragmatic: ignoring losses only prolongs the malaise by creating zombie firms and misallocated capital. The property sector example is illustrative — rolling over bad loans keeps construction crews on payroll for a while but delays reallocation of resources to productive uses. Better to use targeted fiscal support to complete essential unfinished housing, protect vulnerable households, and simultaneously accelerate investment in human capital and new productive capacity. This is politically hard; it requires transparent accounting and acceptance of short-term pain for longer-term, higher-quality growth.

If one statistic frames the coming decade, it is not the headline GDP number. It is the structural fact that the old engines of accumulation are gone and that the country must now pay for past leverage while building new capital on its own balance sheets. The policy implication is stark: stimulus that simply re-creates leverage will postpone recovery; policies that accelerate China's rebuilding capital — by investing in people, conditioning subsidies on performance, and cleaning bank and developer balance sheets — will lengthen the recovery but raise the odds of durable, inclusive growth. Educators should rewire training systems; administrators should link fiscal incentives to measurable capability gains; policymakers should madisclosure andand creditor restructuring a priority. The challenge is long; the prize is an economy that grows slower but on sturdier legs. That is a far better foundation for national prosperity than a rapid rebound built on borrowed time.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Atlantic Council, Jeremy Mark, 2026. China’s property slump deepens—and threatens more than the housing sector. Atlantic Council.

AMRO (ASEAN+3 Macroeconomic Research Office), 2025/2026. China’s economic recovery: Transitioning to high-quality growth. AMRO.

BIS (Bank for International Settlements), 2006/200x. The financial crisis in Japan during the 1990s. BIS Working Paper.

Carnegie Endowment for International Peace, 2025. The relationship between Chinese debt and China's trade surplus. Carnegie Endowment.

IMF (International Monetary Fund), 2025. World Economic Outlook (October 2025). IMF.

MERICS (Mercator Institute for China Studies), Gunter, J.; Brown, A.; Chimits, F.; Hmaidi, A.; Vasselier, A.; Zenglein, M.J., 2025. Beyond overcapacity: Chinese-style modernization and the clash of economic models. MERICS.

Trading Economics / World Bank data synthesis, 2024–25. China GDP and fiscal indicators. World Bank.

Yueh, L., 2026. No easy way out of China’s slowdown. East Asia Forum.

Keith Lee is a Professor of AI/Finance at the Gordon School of Business, part of the Swiss Institute of Artificial Intelligence (SIAI). His work focuses on AI-driven finance, quantitative modeling, and data-centric approaches to economic and financial systems. He leads research and teaching initiatives that bridge machine learning, financial mathematics, and institutional decision-making.

He also serves as a Senior Research Fellow with the GIAI Council, advising on long-term research direction and global strategy, including SIAI’s academic and institutional initiatives across Europe, Asia, and the Middle East.