Silicon Surge, Shallow Base: How Taiwan AI growth Reshaped a Narrow Recovery

David O’Neill is a Professor of AI/Policy at the Gordon School of Business, SIAI, based in Switzerland. His work explores the intersection of AI, quantitative finance, and policy-oriented educational design, with particular attention to executive-level and institutional learning frameworks.

In addition to his academic role, he oversees the operational and financial administration of SIAI’s education programs in Europe, contributing to governance, compliance, and the integration of AI methodologies into policy and investment-oriented curricula.

Authored On

Modified

Taiwan AI growth in 2025 was driven mainly by semiconductor exports Tech demand masked weakness in other sectors across East Asia Long-term resilience now requires broader skills and industrial diversification

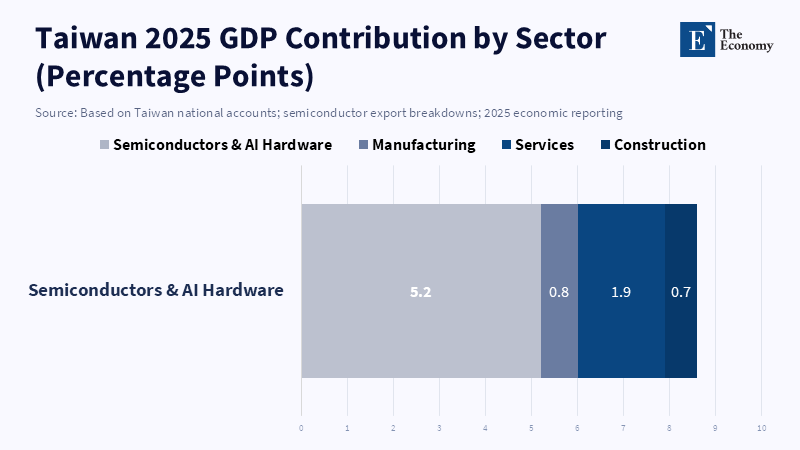

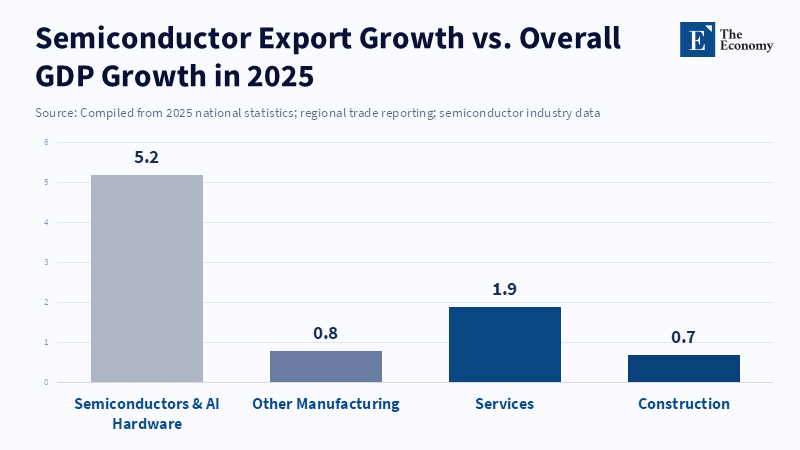

Taiwan’s 2025 bounce was not gradual: gross domestic product jumped into double-digit territory in parts of the year and closed the year with an annual gain that outpaced most peers — a startling sign that AI demand had become the economy’s single most powerful accelerator. The clearest measure is export-led: a concentrated appetite for advanced chips and high-performance computing hardware lifted trade balances and corporate earnings so sharply that a single sector offset long-term declines across other manufacturers. That pattern — exceptional growth driven by a narrow, technology-heavy slice of manufacturing — is what we mean by “Taiwan AI growth”: not broad industrial revival, but a high-value spike anchored in a handful of firms and products. This reframing raises different questions: how resilient is a growth story that depends on one input-intensive, geopolitically exposed industry, and what should educators, universities, and policymakers do when learning ecosystems depend on volatile, export-driven demand?

Taiwan — Taiwan AI growth as a concentrated miracle

Taiwan’s headline numbers look generous until we unpack their anatomy. The island’s 2025 expansion came with two features that matter for policy: extreme export concentration and an outsized share of advanced chips in corporate top lines. Exports surged because global hyperscalers and cloud providers accelerated purchases of AI servers; those purchases required the most advanced back-end fabrication and packaging capabilities that Taiwan specialises in. The result: GDP growth that reads like a national success story but, in truth, is largely a firm-level phenomenon translated into national aggregates.

That concentration matters because it changes both risk and policy levers. When the majority of export surplus and reserve accumulation flows from a handful of capital-intensive fabs, shocks to capital spending, trade policy, or geopolitical access will transmit quickly to national accounts. Taiwan’s foreign exchange reserves rose alongside the surplus, but reserves are insurance, not diversification. The correct policy response is not to cheer the headline but to treat the boom as a window for structural repair: shore up lagging sectors, reform trade links that leave manufacturers exposed to single-market demand swings, and invest the surplus into broader industrial upgrading and human capital.

Finally, the education angle is immediate. A chip-led expansion creates rapid demand for engineers and technicians, but not necessarily for the broad skills that sustain manufacturing ecosystems — skilled electricians, machine repairers, logistics managers, and vocational instructors. According to AP News, Taiwan’s economy saw broad-based growth in 2025, driven largely by the artificial intelligence boom and surging semiconductor demand. That divergence raises equity problems and leaves vocational pipelines hollow. Educators must therefore convert short-term labour pressure into long-term, diversified capacity: retraining schemes, modular certificates for emerging factory roles, and scaled apprenticeships tied to medium-sized firms, not only to elite fabs.

TSMC — The foundry that lifted a country (and the policy fragility that followed)

At the centre of the story is one type of firm and one economic phrase: high-performance computing revenue. In 2025, a majority share of the advanced-node wafer business and the premium pricing for AI chips translated into an unusually large fraction of the national export value. That dynamic is not unique to Taiwan — other economies see similar firm-level effects — but the scale on the island is exceptional. When a single company’s product mix drives more than half of the high-end segment’s margin, national growth can look robust while underlying industrial breadth does not improve.

This concentration creates two policy headaches. First, trade measures or export controls that target a narrow set of technologies or customers can quickly reverse the gains. In 2025, Taiwan benefited from restricted Chinese access to the most advanced nodes while selling heavily to U.S. customers; that geopolitical alignment helped the surge. But such alignment is fragile. Second, domestic imbalances emerge: capital flows, wage inflation in the tech cluster, and skill shortages, all of which can raise costs for non-chip firms. Policymakers should treat the foundry success as seed capital for industrial diffusion: use public co-investment and tax incentives to encourage chip-adjacent industries (testing, packaging, specialty materials) and, crucially, to modernise the lagging assembly, metalworking and machine-tool segments that once formed Taiwan’s industrial base.

For education systems, this implies immediate and medium-term action. Immediate: scale micro-credentials in semiconductor process maintenance, equipment calibration, and data-centre operations, co-designed with fabs and equipment vendors so curricula match skill needs. Medium-term: rebuild vocational institutes around adaptable competencies — diagnostics, industrial IT, and supply-chain analytics — that matter whether the next decade’s premium is chips, batteries, or green hydrogen plants. That is how an economy converts a spike into durable capability.

ASEAN, South Korea, China and Japan — Regional echoes: Korea, Japan and ASEAN tell a consistent story

Across Northeast and Southeast Asia, we find a repeating pattern: semiconductor supercycles lift national aggregates while other sectors lag. In the Republic of Korea, a surge in memory and logic exports improved headline growth but left construction and autos soft; in Japan, pockets of tech strength did not spread widely through traditional manufacturing, which faces competition from cheaper Chinese output. ASEAN economies saw Chinese export expansion squeeze local producers in lower-value manufacturing even as electronics orders shifted across the region. These parallel developments show a common mechanism: concentrated, tech-intensive demand can hide structural weakness elsewhere.

What unites these cases is three shared pressures. First, demand is geographically concentrated (big cloud buyers and a small set of global integrators). Second, supply chains are hyper-specialised (advanced packaging lives in a few clusters). Third, politics and trade policy reshape flows rapidly: tariffs, export controls, and investment screening move demand around faster than labour markets can adapt. For ASEAN, the immediate effect was twin-edged — Chinese exporters redirected output to Southeast Asia while some higher-value supply-chain tasks moved inwards toward Taiwan and Korea. According to a recent report on Taiwan's semiconductor market, the industry's output value is projected to reach NT$ 6.5 trillion (US$ 202.4 billion) in 2025, a 22.2% increase from the previous year, driving record growth at certain factories and ports.

For educators and administrators across the region, the lesson is that training pipelines must be portable and credit-transferable. If a factory in Hanoi suddenly needs test-engineers for server modules, local colleges should be able to offer a 12-week, recognised pathway that sends competent technicians the next month. Regional collaboration can make that feasible: shared curricula, mutual recognition of short certificates, and joint industry boards that specify competency sets. The alternative is slow, costly retraining after demand has moved.

Policy prescriptions for educators and policymakers to keep learning—and growth—broad

First, treat “Taiwan AI growth” as both an opportunity and a risk. Use surplus flows and corporate tax windfalls to underwrite durable public goods: vocational upgrades, teacher retraining, and funded internships that connect mid-tier firms with students. Policymakers should resist the temptation to subsidise only the firms already winning the global race; instead, expand training vouchers for SMEs and technical colleges to improve the middle tier of the supply chain’s productivity and resilience. Public investment in modular, competency-based training yields a higher social return than a transient subsidy to a single export line.

Second, redesign tertiary and vocational credentials for modularity and speed. Short, stackable certificates that map to real tasks — wafer maintenance, data-centre rack installation, thermal systems diagnostics — reduce friction between labor supply and demand. Governments should fund curriculum co-design with firms and certify competence quickly; universities can offer the academic backbone while polytechnics deliver applied skills. This is cheaper and faster than building brand-new degree programs that graduates only after a multi-year lag.

Third, regional cooperation is not optional. ASEAN, Taiwan, South Korea, and Japan should create a compact for skills mobility: reciprocal recognition of short credentials, labour mobility corridors for technicians, and shared emergency recruitment protocols for rapid scale-up. Such mechanisms protect education pathways from the whiplash of global demand. They also embed resilience: when demand shifts, students and workers can follow certified paths rather than fall into long unemployment spells.

The 2025 expansion taught us a paradox: remarkable national performance can hide narrow foundations. “Taiwan AI growth” is real, valuable and globally consequential — but it is not a substitute for broader industrial strength or inclusive workforce development. The immediate challenge for educators and policymakers is to convert exceptional returns into durable capability. That means investing export windfalls in skills, modular credentials, and cross-border recognition schemes; it means focusing teacher development and vocational infrastructure on tasks that matter to the middle of the supply chain; and it means building regional agreements that make skills portable when demand migrates. If we fail to act, the next semiconductor up-cycle will again lift aggregates while leaving students, small firms and communities exposed. If we succeed, the chip boom will seed a more diversified, resilient industrial map — and schools will have played the decisive role.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Asia Society Policy Institute, 2025. Kelly, B. & Wester, S., ASEAN Caught Between China’s Export Surge and Global De-Risking, Asia Society Policy Institute.

Chiang, M.-H., 2026. Taiwan rides the AI wave to rapid economic growth. East Asia Forum.

Economy.ac, 2025. Hansbrough, T., “East Asia’s Three-Way Rivalry Heats Up” — China’s Southeast Asia Push Gathers Pace, Home Manufacturing Faces Growing Strain. The Economy.

Focus Taiwan (CNA), 2026. Pan, T.-y. & Lee, H.-Y., Taiwan economic growth hits 8.63% in 2025, highest in 15 years. Focus Taiwan (CNA).

Ju, S., 2026. Semiconductor boom lifts exports sharply… "Growth likely to continue for 9 straight months", The Asia Business Daily (Asiae).

Min-Hua Chiang (author note: see East Asia Forum contribution), 2026. Taiwan rides the AI wave to rapid economic growth, East Asia Forum.

Reuters, 2025. Hung, F. & Kao, J., Taiwan 2025 GDP growth forecast hits 15-year high on surge in AI demand. Reuters.

The Chosun Ilbo, 2026. Semiconductor Surge Reveals South Korea’s K-Shaped Economy. Chosun Ilbo.

David O’Neill is a Professor of AI/Policy at the Gordon School of Business, SIAI, based in Switzerland. His work explores the intersection of AI, quantitative finance, and policy-oriented educational design, with particular attention to executive-level and institutional learning frameworks.

In addition to his academic role, he oversees the operational and financial administration of SIAI’s education programs in Europe, contributing to governance, compliance, and the integration of AI methodologies into policy and investment-oriented curricula.