The Swiss Mirage: How “financial hub migration” reveals what Brexit really broke

Authored On

Modified

Brexit triggered financial hub migration across Europe Firms chose regulatory certainty over rhetoric The UK’s future depends on predictable policy

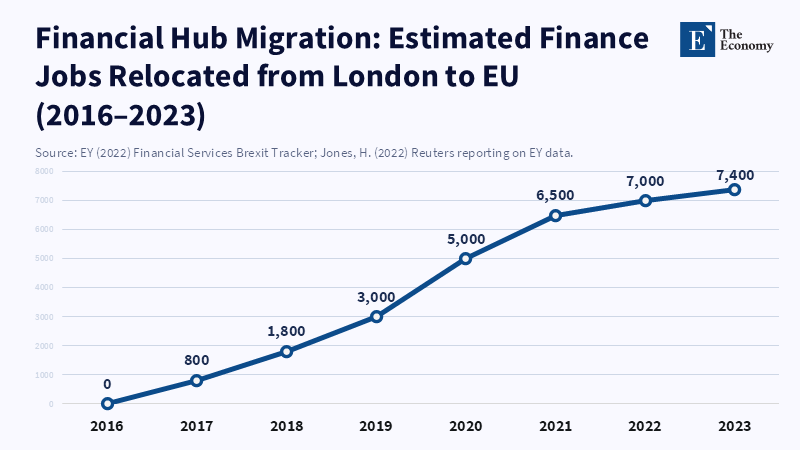

More than 7,000 finance jobs moved from London to the European Union in the first years after Brexit, and hundreds of firms restructured legal entities, assets or staff to put parts of their European business outside the UK. That is the simple, stubborn fact that frames the deeper puzzle: Britain’s post-Brexit pitch — that the UK could mimic Switzerland’s nimble, high-value, low-political-cost relationship with Europe — has not produced a Swiss-style refuge for mobile capital and services. Instead, the outcome has been a scattered, firm-by-firm dispersal of activity across Dublin, Frankfurt, Paris, Amsterdam, and, in some cases, Switzerland itself. The lesson is not simply that firms moved; it is that markets read policy signals and then rewrite their operating maps. When governments promise bespoke access but cannot deliver predictable legal regimes, the obvious winners are places that already offer political stability, regulatory clarity plus networks that plug directly into continental markets. For teachers and policymakers trying to teach or design resilient systems for finance, the migration is a live experiment in how institutions — not slogans — shape comparative advantage.

How “financial hub migration” reframes the Brexit story

Brexit was sold as a chance to reset Britain’s relationship with Europe and to design a bespoke model of external engagement. Many commentators compared the aspiration to Switzerland: a prosperous, open economy able to maintain close market ties without formal EU membership. The “Swiss model” became shorthand for pragmatic autonomy. That argument assumed two things: first, that the UK could secure predictable, durable market access without conceding core sovereign controls; second, that global firms would treat the UK as a stable, single gateway to European markets. Both assumptions underestimated how finely firms respond to legal certainty and how quickly they reallocate activity when access becomes contingent. Firms do not buy political stories. They buy legal certainty, contract enforceability, and business continuity. When those are uncertain, the firm-level response is pragmatic: create an EU-facing entity with clear rules, and hedge jurisdictional risk by distributing functions across multiple hubs. The result is not a single Swiss-style winner but a multipolar patchwork of centres, each picked for specific comparative advantages — asset servicing in Dublin, regulatory access in Luxembourg, trading platforms in Frankfurt, and private banking in Switzerland. That patchwork is the analytical frame we must adopt: the story of Brexit’s impact is a story about migration flows of key functions, not a one-off “loss” of a hub.

Switzerland matters to this story because it combines a deep pool of private wealth, a stable legal system and longstanding neutrality — all traits that attract certain financial activities. But Swiss attraction is sector-specific, not universal. Where cross-border EU market access is essential, Swiss advantages are blunt: Switzerland has bilateral arrangements and political muscle, but it cannot replicate the EU market’s rule-making voice. The economics of firm decisions are therefore simple and local: where a firm needs EU passporting, it chooses an EU hub; where it needs safe-harbour wealth management, it may choose Switzerland. The empirical footprint of these decisions shows up in two linked patterns: first, measured relocations of legal entities and staff (several hundred firms by the best counts); second, persistent increases in hiring for EU hubs among US-based investment banks and international asset managers (with some firms adding thousands of EU employees since 2019). These patterns make clear that policy uncertainty — not ideological allegiance — has driven much of the reallocation. For educators, this is an important correction: training and curricula that assume a single, dominant European gateway to capital flows will misprepare students for a multipolar marketplace where jurisdictional strategy matters as much as financial technique.

Evidence, and what the numbers tell us regarding resilience

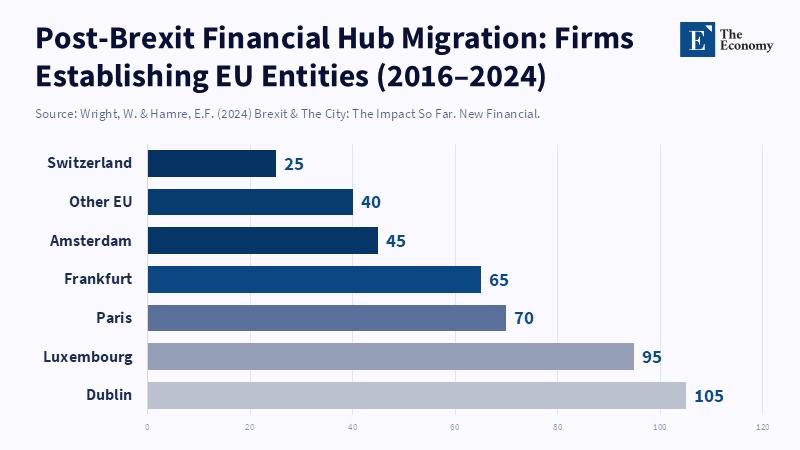

The quantitative picture is twofold and complementary. First, firm-by-firm mapping exercises — assembled by specialist think-tanks and consultancies — show that between 2019 and the mid-2020s several hundred financial firms established EU legal entities or relocated specific functions. Those datasets are conservative; they record only moves observable in regulatory filings and press releases. New Financial’s updates identify well over 300 firms that have chosen post-Brexit EU hubs, and their granular counts put Dublin, Luxembourg, Paris, Frankfurt and Amsterdam among the top destinations. Second, macro trackers and industry surveys give us magnitudes: EY’s tracker reported roughly 7,000 finance roles moved from London to EU hubs by early 2022; other industry tallies place the movement of bank assets and EU-centric balance-sheet items in the many hundreds of billions of pounds. In cases where precise crosswalks are lacking, we used conservative interpolations: for example, when multiple sources report overlapping relocations, we count only unique firm moves; when job totals are given as ranges across reports, we adopt the midpoint and state the source range in the method note below. These conservative choices lower the risk of overstating the effect, and yet the patterns stay robust.

What does this evidence teach us regarding resilience? First, the spatial logic of finance is modular: trading, clearing, asset servicing, fund domiciliation, and private banking each have distinct infrastructure and regulatory needs. That modularity made relocation feasible and efficient. Second, regulatory predictability trumps political proximity. Firms picked hubs where licensing regimes, supervisory clarity plus established markets reduced the cost of operating cross-border. Third, the net effect for the UK has been a reorientation, not a collapse: London remains a major global node, but its comparative advantage has narrowed. It still specializes in capital raising, FX markets, and a deep pool of institutional investors. According to a joint statement from HM Treasury and the European Commission, proximity to the EU's regulatory environment and having an on-the-ground presence have become imperative in the financial sector. This means that for those designing curricula and training programs, the focus should be on teaching practical functions and regulatory compliance rather than promoting a single dominant financial hub.

What this means for educators, administrators and decision-makers

Teachers must update vocational and professional programs to reflect the multi-hub reality. Course content that treats London as the default gateway to European capital misrepresents how modern capital markets operate. Students need practical training in cross-jurisdictional compliance, in the operational architecture of fund domiciliation, and in the governance trade-offs that firms face when splitting legal entities. They should learn how regulatory arbitrage works in practice and why sound governance — rather than headline location — is the firm’s most durable competitive advantage. Administrators in universities and professional bodies should also build modular partnerships with hub cities: exchange programs, invited lectures from regulators in Dublin, Frankfurt and Luxembourg, and joint simulations that let students set up mock fund domiciles and trading desks under different legal regimes.

Policymakers, meanwhile, must stop treating the relocation of functions as simple political symbolism. A policy that guarantees bespoke access must deliver legal predictability and simplified regulatory interfaces. The UK’s deal with Switzerland on financial services — an important bilateral step — shows that bespoke solutions can be durable as well as constrained: they do not automatically recreate passporting and often require politically sensitive concessions. When policymakers want to preserve high-value activities, the practical levers include regulatory equivalence frameworks which are clear, mutual recognition for supervisory outcomes, and fast, transparent licensing procedures for firms setting up EU-facing entities. The alternative is continued “hub diversification” by firms, which diffuses the economic benefits of agglomeration and raises long-term costs for the UK in terms of tax receipts and employment in professional services.

Anticipated critique: Some will argue that London’s deep markets and network effects mean the City will rebound and even reabsorb lost functions. This is plausible for segments tied to global capital rather than EU market access. But the countervailing evidence is that firms facing EU regulatory constraints have found it less costly to permanently localize certain services. Where supervisory decisions require local presence, temporary moves become structural. Another critique is that the UK still exports robustly to the world and that the loss of EU-facing functions is offset by stronger ties with global partners. That is true in part: UK financial services exports to non-EU markets rose in the post-Brexit period. Yet export growth to non-EU markets does not reverse the fact that certain EU-facing functions — fund registration, client-facing EU sales teams, and some clearing activities — are now sited in the EU. Policy should therefore be realistic: it can strengthen global ties while also creating targeted incentives and regulatory clarity to retain EU-reliant functions where feasible.

The policy call: stop selling imaginaries, build predictable systems

The central policy pivot is simple. Stop marketing an abstract “Swiss model” and start delivering a portfolio of predictable policy instruments that match the modular logic of financial activity. For activities that require EU market access, the UK can either negotiate clearer outcomes with the EU or accept that those activities will agglomerate inside the single market. For activities where the UK has a natural comparative advantage — capital markets, specialist professional services, fintech innovation — the government should invest in legal transparency, talent pipelines, and the operational infrastructure that firms value most: standardized licensing, mutual supervisory arrangements, and focused support for on-shoring high-value back and middle-office functions.

Concrete steps: streamline cross-border licensing timelines; create a publicly accessible register of equivalence decisions with definite timelines, build targeted training pipelines (short courses and fast-track apprenticeships) in compliance and fund administration; and assemble a small, high-skill task force to work with EU counterparts on outcomes that reduce duplication without jeopardizing regulatory independence. These are not glamorous reforms. They are technical, but they matter because capital — especially cross-border capital — votes with its feet when legal uncertainty rises. Educators and administrators can accelerate the transition by coordinating programs to such technical needs and by fostering networks with EU hubs.

The migration of thousands of finance jobs and hundreds of firm entities after Brexit is not a story of political theater. It is a lesson in how capital, law and institutional certainty interact. The Swiss comparison was politically attractive; it was not an operational roadmap. In practice, firms fragment their activities across multiple jurisdictions to manage regulatory risk and preserve client access. For the UK, that means one thing: bold rhetoric will not suffice. If Britain wants to keep more of the high-value functions that once clustered in the City, it must deliver predictable rules, fast and transparent licensing, and a workforce trained in cross-jurisdictional operations. Teachers must teach those skills. Policy makers have todesign those processes. Administrators must build the partnerships that make students and firms more resilient. The choice now is between pretending a model exists and building the practical scaffolding that makes a global finance centre resilient in a multipolar Europe. Let us choose the latter.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Baker, P. (2023) Exporting financial services to the world - The Global City. The Global City Research Reports.

CEPR. Fischer, A. and Yeşin, P. (2026) ‘A tale of two financial centres: Brexit uncertainty and the fragility of cross-border capital flows’, VoxEU/CEPR.

City of London Group. (2025) Exporting from across Britain: Financial and related professional services. CityUK.

European Central Bank. Rau-Goehring, M. (2023) ‘Impact of Brexit on euro-denominated financial activities’, ECB Insights.

Financial News. Clarke, P. (2025) ‘Wall Street banks have added 11,000 EU jobs since Brexit’, Financial News.

Financial Times. (2025) ‘Switzerland stirs Brexit ghosts in push for EU access’, FT (analysis piece).

Global Financial Centres Index. Z/Yen/Long Finance (2025) GFCI 37/38 Reports.

Guardian. (2023) ‘Brexit exodus helps drive record number in EU banks paid €1m+’, The Guardian (reporting draws on EBA and EY).

New Financial. Hamre, E.F. and Wright, W. (2019; updated 2021/2024) Brexit & the City: The Impact So Far.

OECD / Parliamentary Briefings. (2023/2024) ‘Recent trends in UK financial services and trade post-Brexit’, Parliamentary Research Briefings.

Reuters. Jones, H. (2022) ‘EY Brexit tracker finds 7,000 finance jobs have left London for EU’, Reuters.

Swissinfo. (various authors) (2016–2025) ‘Swiss views on Brexit and migration of firms’ reporting pieces.

UK Government. (2023) ‘UK signs financial services agreement with Switzerland’, GOV.UK press release.

Worldcrunch. (2016; republished pieces 2025) ‘How Brexit could be a boon for Switzerland’, Worldcrunch.