U.S. Treasury Yields Break Above 4%, Signaling Liquidity Strain as War, Oil, and Rates Drive Market Into Wait-and-See Mode

Authored On

Modified

Volatility Expands Even in Treasuries Once Seen as Safe Assets

Redemption Pressure Exposes Fragility in Private Credit Liquidity

Risk Aversion Intensifies, Deepening Market Tightness

As U.S. Treasury yields surge past 4% in the wake of the Middle East war, tensions are rising across global financial markets. Alongside higher yields, demand for bonds has weakened and trading liquidity has sharply deteriorated, triggering warning signals in the world’s largest government bond market. With prolonged conflict and rising energy prices converging, expectations for the monetary policy path have been significantly disrupted. Coupled with growing instability in private credit markets, investor caution is spreading across the broader market.

Fading Ceasefire Hopes → Sharp Decline in Bond Prices

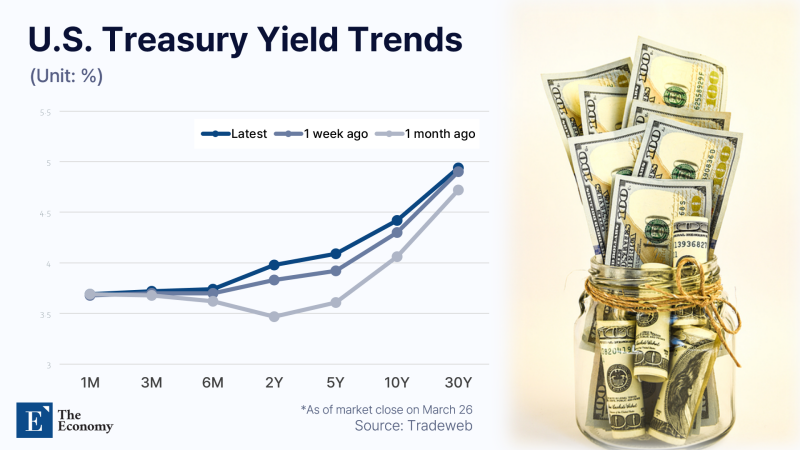

According to electronic trading platform Tradeweb on March 26, the yield on the 10-year U.S. Treasury rose to 4.42% near the close of the New York session, up 0.09 percentage points from the previous day. The yield on the policy-sensitive 2-year Treasury also climbed 0.12 percentage points to 4.00%. As uncertainty stemming from the Iran conflict fuels expectations that the Federal Reserve will find it difficult to cut rates, weak demand at a 7-year Treasury auction held the same day further accelerated the sell-off in bonds.

Markets are increasingly concerned about a breakdown in liquidity. According to the Financial Times, “market depth” in the approximately $30 trillion U.S. Treasury market has fallen to less than half its level over the past month, indicating a sharp decline in the market’s ability to absorb large orders at specific price levels. Conditions in the short-term Treasury futures market are even more severe. Market depth there is estimated to have dropped by as much as 80% compared to the annual average, a level of shock comparable to April of last year when Donald Trump announced sweeping global tariff policies.

Signs of strain have also emerged on trading desks. On March 23, major Wall Street banks simultaneously halted their automated quoting systems, which typically operate around the clock. The move followed a sharp spike in price volatility after Trump stated that the U.S. had engaged in “productive talks” with Iran, only for Iranian officials to deny the claim. Bid-ask spreads widened significantly, prompting dealers to shift from automated systems to direct trader-to-trader negotiations. Such disruptions in liquidity provision mechanisms underscore growing instability at the core of the bond market.

At the heart of rising yields lies energy prices. As prolonged conflict drives up global oil prices, renewed inflation concerns have emerged, rapidly reversing expectations for monetary policy. The 2-year Treasury yield has risen by 0.62 percentage points so far this month, marking its largest monthly increase since September 2022. Just a month ago, rate futures markets had priced in two to three rate cuts within the year; now, the possibility of additional rate hikes is being reflected in pricing.

Top Asset Managers Struggle With Redemption Pressures

Another headwind comes from private credit risks. Recently, large-scale redemption requests at major private credit managers have heightened market anxiety. Ares Management, the world’s largest private credit manager, received redemption requests equal to 11.6% of net assets in its Ares Strategic Income Fund but capped withdrawals at 5%. Apollo Global Management also imposed similar limits after facing redemption requests of 11.2% in its funds. Meanwhile, Blue Owl Capital’s technology-focused fund recorded quarterly redemptions of around 15%.

The concern is that such pressures can lead to price distortions and heightened credit risks. Blue Owl sold $1.4 billion in loans at approximately 99.7% of face value to secure liquidity, but markets interpreted the move not as a routine transaction but as a signal of risk aversion. Subsequently, Blue Owl’s stock fell for 11 consecutive trading sessions, erasing roughly 60% of its market capitalization, while some fund stakes were subject to tender offers at a 33.2% discount to net asset value. Around the same time, Moody’s downgraded another major manager, KKR’s private credit fund, to speculative grade, reinforcing concerns over credit risk.

This structure amplifies liquidity stress. Private credit, while based on illiquid assets, often allows quarterly redemptions, meaning concentrated withdrawal demands can trigger simultaneous asset sales and price declines. This dynamic raises the risk of deteriorating credit quality in a rising rate environment. Some observers have even drawn parallels to the period preceding the 2008 financial crisis, suggesting that private credit risks, combined with liquidity stress in the Treasury market, could heighten systemic credit tightening across financial markets.

Sharp Deterioration in Investor Sentiment

Markets have broadly shifted into a wait-and-see mode. With little visible progress in ceasefire negotiations between the U.S. and Iran, investors are increasingly factoring in the possibility of further escalation. While Israel’s Channel 12 reported that the U.S. had proposed a one-month ceasefire along with 15 conditions, The New York Times interpreted the proposal as a broader peace plan, highlighting conflicting narratives around the negotiations. This uncertainty is precisely what markets find most unsettling. When the trajectory of war and the nature of negotiations remain unclear, yields, oil prices, and risk asset valuations can swing dramatically on a daily basis, prompting investors to prioritize cash holdings and reduced trading activity over aggressive positioning.

Adding to this caution is the uncertainty surrounding private credit. Market participants are particularly concerned about the opaque size of the sector, the distribution of potential losses, and its connections to the broader financial system. Unlike assets with daily price discovery, private credit markets are thinly traded with infrequent valuation cycles, making it difficult to determine when losses may surface. In a high-rate environment, borrowers face accumulating interest burdens, and if prolonged conflict drives up costs and funding pressures, credit concerns could escalate rapidly.

However, there remains some caution against equating current conditions directly with a systemic crisis like that of 2008. Private credit exposure is diversified across sectors such as AI, software, healthcare, industrials, and consumer goods, reducing the likelihood of a single-point collapse similar to the subprime mortgage crisis. Nevertheless, markets remain uneasy because pricing is increasingly factoring in potential credit deterioration before the actual scale of losses becomes clear.

Ultimately, the prevailing market strategy at present leans toward defensive positioning rather than directional bets. While many analysts do not view the equity market correction as being driven by deteriorating corporate earnings, the interplay of oil prices, interest rates, and supply disruptions creates an environment where managing volatility takes precedence over expansion. With neither the timeline of ceasefire negotiations nor the true scope of private credit risks clearly defined, global markets are likely to remain in a cautious phase, prioritizing liquidity and reduced exposure over premature optimism.

Similar Post